Crude Realities: Why the U.S. Imports Oil Despite Leading Production

Refined Choices: The Hidden Reasons Behind U.S. Oil Imports

TL;DR

Why the U.S. Imports Oil: Despite being a top crude oil producer, the U.S. imports oil due to its refineries being historically configured to process sour and medium crude oils, which differ from the light, sweet crude produced domestically. This blend optimizes refinery operations, meets diverse product demands, and ensures cost efficiency.

Refining Infrastructure Challenges: U.S. refineries were built for imported crude during an era of heavy reliance on foreign oil. Adapting to process domestic sweet crude requires costly retooling, involving changes to distillation, cracking, and desulfurization units—an investment that most refineries find prohibitive without government support.

Shale Revolution's Impact: The shale boom has made the U.S. the largest global crude oil producer and a net exporter of crude and refined products. However, the mismatch between refining capabilities and domestic production necessitates continued imports of heavier crude for blending and optimal refinery utilization.

Barriers to Retooling: Retooling refineries to exclusively process sweet crude faces significant regulatory and financial hurdles. Without subsidies, tax incentives, or loans, the economic case for such an overhaul is weak, making complete energy independence or the envisioned "energy dominance" that the incoming Trump administration seeks unlikely.

Strategic Position: The U.S. remains a global energy leader, benefiting from its advanced refining infrastructure and ability to export refined products. Achieving true energy independence and especially “energy dominance” will require balancing refinery adaptation costs, regulatory challenges, and evolving market demands.

Introduction:

The United States is a global leader in crude oil production, yet it continues to import substantial amounts of oil from foreign countries. This apparent contradiction is not merely a matter of supply and demand but rather a reflection of the complexities of the oil refining industry, the diversity of crude oil types, and the historical configuration of U.S. refineries. Understanding why the U.S. imports oil despite its significant domestic production involves exploring concepts like "foreign crude dependency," the mechanics of refining, and the unique characteristics of U.S. refinery infrastructure. Additionally, the nation's energy policies, economic strategies, and the challenges of adapting to a changing energy landscape further illuminate the reasons behind this seemingly paradoxical practice.

This exploration begins with a look at the definitions of "foreign crude dependent," "crude independent," and "net crude exporter" to provide context for how countries, including the U.S., navigate energy security. From there, the discussion delves into the workings of refineries, the role of crude oil types in refining processes, and the impact of the shale revolution on U.S. oil production. By examining the dynamics of U.S. refineries, the shift from sour to sweet crude, and the challenges of retooling refinery infrastructure, this analysis sheds light on the intricate interplay of market forces, technological considerations, and policy decisions that shape America's oil import and export strategies.

“Foreign crude dependent” versus “crude independent” versus “net crude exporter”

The concept of "foreign crude dependent" refers to a country or region that relies on importing crude oil from other nations to meet its domestic demand. This dependency can arise due to a lack of sufficient domestic oil production, or because domestic production does not match the quality or type of crude needed by its refineries. Countries in this category often face risks related to geopolitical tensions, shipping disruptions, or price volatility in the global oil market, as their economy and industries are directly affected by external supply conditions.

On the other hand, "crude independent" describes a scenario where a country produces enough crude oil to meet its own consumption needs without needing to import. This independence can provide a buffer against international market fluctuations and supply disruptions. Being crude independent means that a nation's energy security is less vulnerable to external factors, although it might still be influenced by global price changes.

Lastly, a "net crude exporter" is a country that not only meets its own demand for crude oil but also has surplus production which it can sell on the international market. This may be due to the outcome of domestic production does not match the quality or type of crude needed by its refineries. This position can offer economic advantages, contributing to foreign exchange earnings and often strengthening the country's geopolitical influence. Countries that are net exporters might use this status strategically to leverage international relations or to stabilize or manipulate global oil prices to their benefit. However, this status also comes with the responsibility of managing production to avoid market oversupply which could depress prices, affecting their revenue.

Each of these statuses reflects different levels of energy security, economic strategy, and international influence, shaped by a nation's natural resources, technological capabilities, and policy decisions.

Brief explanation of how refineries work

Refineries are complex industrial plants designed to transform crude oil, a raw natural resource, into a variety of useful products like gasoline, diesel, jet fuel, heating oil, and various petrochemicals used in plastics, pharmaceuticals, and countless other products. The process begins when crude oil, which is a mixture of hydrocarbons, is transported to the refinery where it is first stored in large tanks.

The initial step in refining is the separation of crude oil into different components based on their boiling points through a process called distillation. In the distillation unit, often referred to as the atmospheric distillation tower, crude oil is heated in a furnace to temperatures around 350-400 degrees Celsius. As the heated oil enters the bottom of the tower, it vaporizes. The vapors rise up the column, cooling as they ascend, and condense at different heights based on their boiling points. Lighter hydrocarbons like gasoline and naphtha condense at the top, while heavier components like diesel and lubricating oils are collected at lower levels.

However, the fractions obtained from simple distillation are not yet in their final form for consumer use. They undergo further processing in various units. For example, the heaviest fractions, which are not suitable for direct use, go through a cracking process. Cracking, or conversion, breaks down larger, heavier hydrocarbon molecules into smaller, lighter ones. This can be done through thermal cracking, where heat alone is used, or catalytic cracking, which uses a catalyst to speed up the reaction at lower temperatures, yielding more valuable products like gasoline.

After cracking, there is often a need to enhance the quality of the products. This involves processes like alkylation, where light olefins from the cracking process are combined to form high-octane gasoline components, or hydrotreating, where hydrogen is used to remove impurities like sulfur and nitrogen, improving the product's environmental impact and performance.

The final stages include blending, where different streams of hydrocarbons are mixed to meet specific product specifications like octane rating for gasoline or viscosity for lubricants. Additives might also be incorporated at this stage to improve fuel performance, reduce emissions, or meet regulatory standards.

Throughout this process, refineries manage waste and by-products, often recycling or converting them into other useful materials or energy, striving for efficiency and environmental compliance. The operation of a refinery is a delicate balance of chemistry, engineering, and economic considerations, constantly adapting to both the quality of incoming crude and the demand for different refined products in the market.

US Refineries

The United States has 132 operable petroleum refineries as of January 1, 2024. These refineries collectively process a significant amount of crude oil, contributing to the nation's energy supply. The combined refining capacity of these facilities is approximately 18.4 million barrels per day, which makes the U.S. one of the world's leading countries in terms of refining capacity. This capacity has seen fluctuations over the years, with a general trend of increasing complexity and efficiency in the operations of these refineries, even as the number of facilities has decreased from historical highs.

The largest refinery in the United States, as of 2024, is the Marathon Petroleum facility located in Galveston Bay, Texas, with a refining capacity of 631,000 barrels per calendar day. This significant capacity underscores the strategic importance of Texas in the U.S. refining landscape, where many of the country's largest refineries are situated due to the proximity to both crude oil production sites and major shipping routes. The scale of this refinery allows it to produce a wide range of petroleum products, from gasoline to diesel, jet fuel, and various petrochemical feedstocks, catering to both domestic and international markets.

The output statistics reflect not only the capacity for crude oil distillation but also the capability of these refineries to convert crude oil into a variety of products that meet diverse consumer and industrial needs. This involves complex processes like cracking, reforming, and hydrotreating, which enhance the yield of high-demand fuels and reduce the environmental impact of the refined products. The operations of U.S. refineries are pivotal in influencing fuel prices, supply stability, and the country's position in global energy markets. However, these statistics can vary slightly year over year due to maintenance schedules, expansions, or closures of refineries.

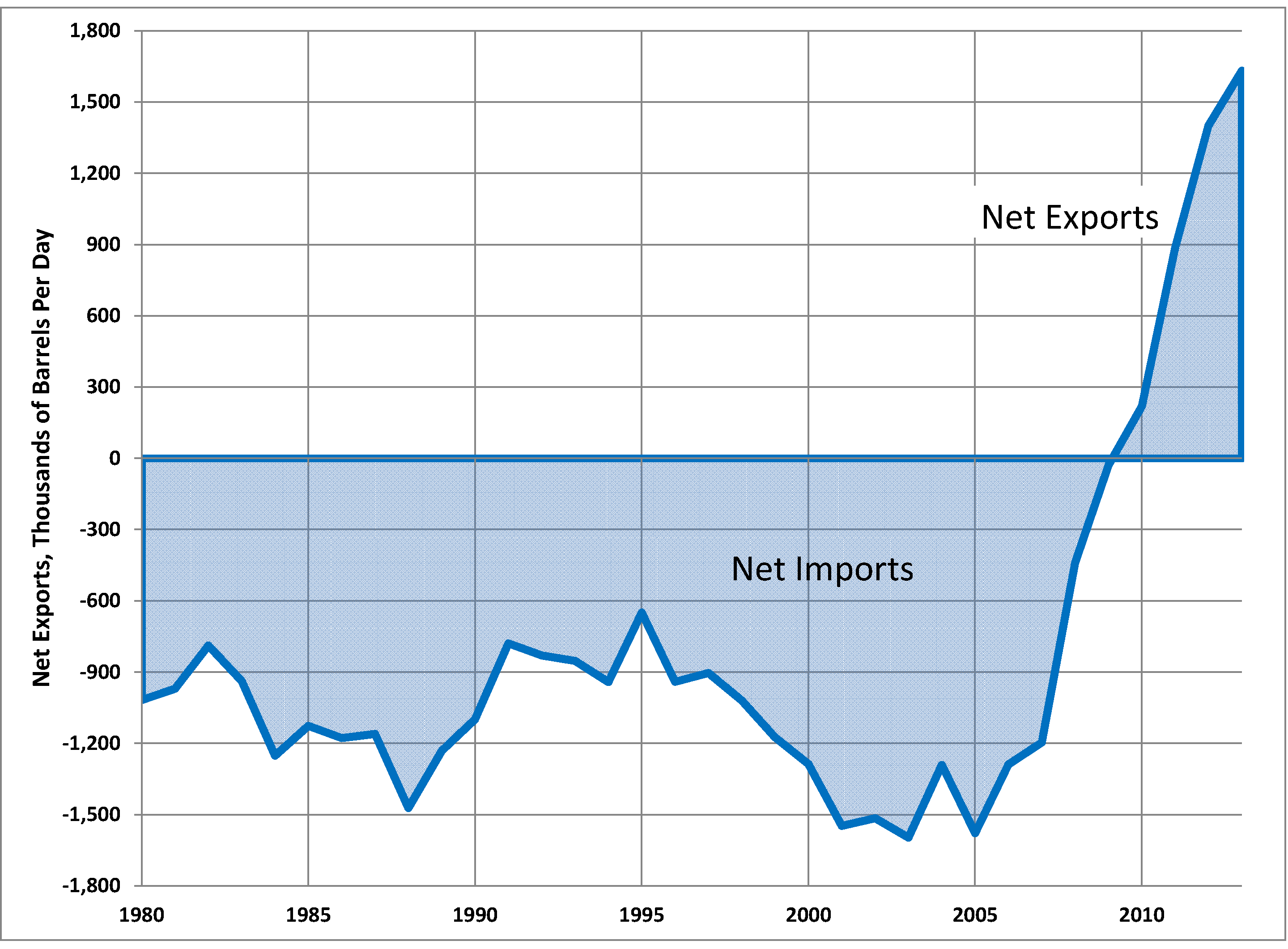

The United States has become the largest exporter of refined oil products in the world. This significant shift occurred sometime between 2011 and 2013 depending on how you measure this, when the US surpassed Russia to claim the top spot in exporting refined petroleum products like gasoline, diesel, and jet fuel. This transition was facilitated by a surge in domestic oil production, particularly from the shale boom, which provided an ample supply of crude oil to refineries. Additionally, the US benefited from having one of the world's most advanced and extensive refining infrastructures, which allowed it to process not only domestic crude but also imported crude into high-demand refined products.

The peak in US exports of refined oil products has been supported by various factors, including increased refining capacity, technological advancements in refining processes, and strategic geographical positioning that allows easy access to both domestic and international markets. By 2022, the US was exporting around $138 billion worth of refined petroleum, making it the leading exporter globally. This growth in exports reflects the country's energy policy changes, including the lifting of the crude oil export ban in late 2015, which indirectly encouraged more refining and export activities.

(Pictured above: Net US exports (exports minus imports) of refined petroleum products, 1980-2013. Data from OPEC)

The US's status as the largest exporter of refined oil products is also influenced by the dynamics of global energy markets, where demand from countries like Mexico, Canada, and Brazil has been significant. The ability to refine a variety of crude oils into products tailored to different market specifications has given US refineries a competitive edge. This export dominance is not just a testament to the volume of production but also to the efficiency and adaptability of the US refining sector to global energy needs. However, this position can be subject to change based on global oil prices, geopolitical events, and shifts in domestic and international energy policies.

The contribution of oil refining to the U.S. GDP is significant but varies year by year due to fluctuations in oil prices, production levels, and the broader economic context. According to the American Petroleum Institute, the oil and natural gas industry, which includes refining, contributes nearly 8 percent of the U.S. GDP. Specifically focusing on refining, it represents a subset of this broader category.

More precise data from the U.S. Energy Information Administration (EIA) and other sources suggest that the refining sector alone directly accounted for about 1.8% of GDP in 2015, according to the Bureau of Economic Analysis data cited in various reports. However, when considering the broader impact, including indirect contributions through activities like transportation, manufacturing of oil products, and support industries, the figure rises. Plus, that is a 2015 figure and it is likely much more given current production levels.

A refinery is not a refinery for all

Refineries are designed with specific configurations that optimize the processing of particular types of crude oil, categorized mainly by their sulfur content and gravity (light, medium, heavy). Crude oil types like sour, sweet, or medium each have distinct properties that dictate how a refinery must be set up to handle them effectively.

"Sweet" crude oil has low sulfur content, making it less corrosive and easier to refine into high-value products like gasoline. Refineries set up for sweet crude typically have less extensive desulfurization equipment since there's less sulfur to remove. They might focus more on units like catalytic crackers for gasoline production or hydrocrackers to maximize yield from the lighter fractions of the crude.

Sweet crude oil, characterized by its low sulfur content (less than 0.5% by weight), is considered the easiest and least expensive type of oil for refineries to process into various products for several reasons. Firstly, the low sulfur content means that sweet crude is less corrosive to refining equipment. This reduces the wear and tear on machinery, lowering maintenance costs and extending the lifespan of the refinery's infrastructure. Without the need for extensive desulfurization, refineries can avoid the capital and operational expenses associated with installing and maintaining sulfur removal units like hydrodesulfurization (HDS) units.

Secondly, sweet crude naturally contains a higher proportion of light hydrocarbons, which are easier to refine into high-value products such as gasoline, diesel, and jet fuel. These lighter fractions require less processing in terms of cracking or hydrotreating to achieve the desired product specifications. This simplicity in refining translates into lower energy consumption, as the crude doesn't need to undergo as many high-energy processes to break down heavier molecules or remove impurities.

Moreover, the refining process for sweet crude generally involves fewer steps. Since there is less sulfur to deal with, there is less need for complex treatment processes to meet stringent environmental regulations concerning sulfur emissions. This not only reduces operational complexity but also decreases the environmental footprint of refining, which can be advantageous in terms of regulatory compliance and public perception.

The ease of processing sweet crude also means that refineries can focus more on optimization for yield, rather than on mitigating the negative effects of sulfur. This can lead to higher throughput rates and better conversion efficiencies, making the overall refining operation more cost-effective. Additionally, sweet crude often yields a higher percentage of high-demand products directly from the distillation process, reducing the need for secondary conversion units, which again cuts down on costs.

In summary, the combination of lower equipment maintenance, reduced energy consumption for processing, less need for environmental treatment, and a natural predisposition towards producing valuable end-products makes sweet crude the least expensive and easiest type of oil for refineries to convert into marketable fuels and chemicals.

"Sour" crude, on the other hand, contains high amounts of sulfur, which is corrosive and can damage refinery equipment if not properly managed. Refineries designed to process sour crude need sophisticated desulfurization units, such as hydrodesulfurization (HDS) units, where hydrogen is used to react with sulfur compounds to remove sulfur, producing hydrogen sulfide which is then converted to elemental sulfur. These refineries also need materials resistant to sulfur corrosion, and their processes include more steps for treating the crude to meet environmental standards.

"Medium" crude refers to its API gravity, which is a measure of crude oil's density compared to water. Medium crudes (like Arab Medium) fall between light and heavy, providing a balance of light and heavy hydrocarbons. Refineries set for medium crude need to have a balanced approach, often with capabilities for both cracking heavier fractions into lighter products and for upgrading lighter fractions. However, they might not have the extensive sour crude handling capabilities if the medium crude is also sweet or has moderate sulfur content.

The challenge with refining different types of crude lies in the specificity of the equipment and processes. If a refinery is optimized for sweet crude, introducing sour crude can lead to equipment corrosion, higher maintenance costs, and reduced efficiency due to the need for additional desulfurization. Conversely, a refinery configured for sour crude might not economically process sweet crude since its desulfurization units would be underutilized, potentially making the process less efficient. Refineries can adapt through modifications or upgrades to process different crudes, but this involves significant capital investment, reconfiguration of units, and sometimes a complete overhaul of the refining strategy. Thus, while it is technically possible to adjust for different crude types, doing so without substantial changes can lead to inefficiencies or even damage to the refinery's infrastructure.

The “set up” of US refineries

U.S. refineries have been historically configured to process sour or medium crude oils rather than sweet crude, a setup that largely reflects the oil import patterns from decades past when the U.S. relied heavily on foreign oil, particularly from the Middle East and Venezuela. During the mid-20th century and well into the 1990s and early 2000s, the U.S. imported substantial amounts of crude oil, much of which was sour or medium grade. This was due to the availability, cost-effectiveness, and the strategic relationships with oil-producing countries like Saudi Arabia, Iraq, Iran, and Venezuela, which predominantly produced these types of crude.

Sour crude from these regions typically contains higher sulfur content, making it less expensive on the global market but more challenging to refine due to the need for additional processing to remove sulfur. To handle this, U.S. refineries invested heavily in technologies like hydrodesulfurization units and coking, which are specifically designed to deal with high sulfur content and heavy hydrocarbons. These refineries were built with infrastructure that could process the heavier, more sulfurous crude into usable products like gasoline, diesel, and jet fuel, which required additional steps like cracking and hydrotreating to meet product quality standards.

The focus on sour and medium crude was also an economic decision at the time. Investments in refining capacity were made based on the assumption that this trend would continue, with the U.S. potentially facing an oil supply dominated by heavier, sour crudes from abroad. Refineries were thus optimized to take advantage of these cheaper crude inputs, which could be processed into higher-value products at a competitive cost. However, this setup meant that when the U.S. experienced its shale oil boom, which predominantly produced light, sweet crude, many refineries were not immediately well-suited to handle this new abundance of domestic oil without significant modifications or investments.

The mismatch between the type of crude U.S. refineries were set up to process and the new reality of domestic oil production has led to a situation where much of the light, sweet crude produced in the U.S. is either processed less efficiently by existing refineries or exported to regions where refining infrastructure is better suited for it. This historical artifact of refinery configurations tailored for a past era of oil import dependency now presents both challenges and opportunities for adaptation in the U.S. refining sector, as it navigates the shift towards more domestic production of lighter, sweeter crude oils.

The Shale Revolution

The United States has significantly increased its crude oil production since the advent of the shale revolution. As of August 2024, U.S. crude oil production reached 13.4 million barrels per day (bbl/d), showcasing the country's dominance in global oil production. This figure represents a historical peak, largely attributed to the shale oil boom that began in earnest in the mid-2000s. Before this revolution, U.S. crude oil production had been on a downward trend, hitting a low of about 5.0 million bbl/d in 2008. The introduction of advanced drilling techniques like horizontal drilling and hydraulic fracturing allowed access to previously uneconomical shale oil reserves, leading to a dramatic turnaround in oil production. By 2019, the U.S. had produced 12.3 million bbl/d, making it the world's top crude oil producer, a title it has maintained since then.

The shale revolution has been particularly impactful in states like Texas and North Dakota. In Texas, the Permian Basin has been central to this surge, contributing significantly to the national output. According to EIA data, the Permian Basin alone was producing over 6 million bbl/d in 2023. Similarly, North Dakota's Bakken Formation has seen substantial growth in oil production since the shale boom, with the state's output reaching about 1.2 million bbl/d by the end of 2023. These regions highlight how the U.S. has leveraged its shale resources to not only meet domestic demand but also to become a major player on the world stage.

Regarding crude oil exports, the U.S. became a net exporter of crude oil in late 2019, a milestone not reached since the 1950s. This shift was facilitated by the lifting of the U.S. crude oil export ban in 2015, coupled with the shale boom's increased production. By 2023, U.S. crude oil exports hit a record high, with exports averaging around 4.6 million bbl/d. This was a significant increase from just 1.2 million bbl/d in 2015, before the export ban was lifted. The U.S. has since solidified its position as one of the world's largest crude oil exporters, with exports in 2024 continuing to reflect this upward trend, although exact numbers can fluctuate with global demand, oil prices, and domestic policy changes.

These statistics underline the profound impact of the shale revolution on U.S. energy landscape, transforming the country from a major importer to a leading exporter of crude oil, significantly altering global energy dynamics. The increase in domestic production has not only reduced reliance on foreign oil but has also allowed the U.S. to influence global oil markets more directly than ever before.

Why we import oil at all

We need to import non-sweet (sour or medium) crude oil to blend with our sweet crude in the U.S. This need stems from the design and capabilities of the country's refining infrastructure, which has historically been optimized for processing heavier, more sulfurous crudes. U.S. refineries, especially those built or significantly expanded during times when the U.S. was heavily dependent on Middle Eastern and Venezuelan oils, were equipped with sophisticated units like cokers, hydrocrackers, and desulfurization facilities specifically tailored to handle sour and medium crude oils. These refineries can economically convert these types of crude into a broad range of products, including gasoline, diesel, and jet fuel.

The shale revolution has led to an abundance of light, sweet crude oil domestically, which, while excellent for some refining processes, does not perfectly match the processing capabilities of many existing U.S. refineries. Sweet crude, with its low sulfur and light nature, yields a high percentage of lighter products right from distillation, but it might not fully utilize the more complex refining units designed for heavier, sour crudes. Blending sweet crude with imported sour or medium crude allows these refineries to:

Optimize the use of their existing infrastructure by ensuring there's enough heavy feedstock for cracking units, which turn heavy hydrocarbons into lighter, more valuable products.

Maintain efficiency in desulfurization units, which would be underutilized if only sweet crude were processed, thus justifying the initial investment in these facilities.

Achieve a balanced slate of products. Blending can help in producing a mix of products that meet market demand, including heavier products like fuel oil or asphalt, which are less abundant in sweet crude.

Furthermore, blending can also be economically advantageous. Sour crude is often cheaper on the global market due to its higher sulfur content and the additional processing it requires. By blending it with sweet crude, refineries can lower their overall feedstock cost while still producing high-quality products. This strategy also aids in maintaining refinery throughput, ensuring that the complex and costly infrastructure operates at or near capacity, which is crucial for profitability.

In essence, the blend of sweet and non-sweet crude oils allows U.S. refineries to leverage their existing capabilities, meet diverse market needs, and maintain economic viability in a landscape where the type of crude oil available has significantly changed due to domestic shale production.

Transition from Sour to Sweet

The transition of U.S. refineries from processing a mix of sour, medium, and sweet crude oils to focusing primarily on sweet crude involves significant physical and mechanical changes. This shift is largely driven by the abundance of domestic light, sweet crude from the shale revolution, necessitating adaptations to optimize refining processes for this type of oil.

Physically, one of the primary changes involves reconfiguring the distillation units. Refineries traditionally designed for sour or medium crude have larger, more complex atmospheric and vacuum distillation columns to handle heavier fractions. For sweet crude, which has a higher yield of lighter hydrocarbons, these units might need resizing or upgrading to better separate the lighter fractions. This could mean modifying the internals of the columns, like changing the trays or packing, to accommodate the different boiling points of sweet crude components. An example of this is the Valero Energy Corporation's McKee Refinery in Texas, where they have invested in upgrading their distillation columns to handle more light sweet crude from the Permian Basin, enhancing efficiency and yield for lighter products.

Mechanically, refineries need to scale back or repurpose desulfurization units since sweet crude has significantly less sulfur. Units like hydrodesulfurization (HDS) that were critical for processing sour crude might be underutilized or repurposed. For instance, Marathon Petroleum has been known to adjust its operations at various refineries to better accommodate sweet crude, which has led to some HDS units being used less intensively or adapted for other processes like hydrocracking, which is beneficial for sweet crude to produce higher octane gasoline components.

The cracking units, particularly fluid catalytic crackers (FCCs) and hydrocrackers, might also require modifications. Sweet crude naturally contains more light hydrocarbons, which can reduce the need for extensive cracking. However, to maximize value, refineries might focus on catalytic reforming to improve gasoline octane ratings or hydrocracking to convert lighter fractions into more valuable products like diesel or jet fuel. An example is the BP Whiting Refinery in Indiana, which, while not exclusively for sweet crude, has seen upgrades to its FCC to handle the lighter feedstocks from shale oil.

Moreover, the logistics of crude oil handling must be reevaluated. Pipelines, storage tanks, and blending facilities might need reconfiguration or expansion to handle sweet crude's different characteristics, such as lower viscosity and corrosivity. This involves not just physical changes but also operational adjustments in how crude is received, stored, and batched for processing. The shift in the refining diet at PBF Energy's Chalmette Refinery in Louisiana included investments in infrastructure to better process light sweet crude, reflecting these logistical adjustments.

Finally, the transition also involves a significant overhaul in operational strategies, including workforce training for new processes, adjustments in maintenance schedules due to the different wear patterns of equipment when processing sweet crude, and recalibration of control systems to manage the different feedstocks. These efforts are part of broader industry trends seen in surveys by consulting firms like Varis Consulting, which noted U.S. refineries' capacity to adapt to more light, sweet crude processing.

In summary, transitioning to sweet-only refining is a multifaceted endeavor requiring both physical alterations to the refinery's core processing units and mechanical adjustments to auxiliary systems, all underpinned by strategic operational changes to maximize the value of the lighter, less sulfurous crude oil now abundant in the U.S.

Retooling in a nutshell

Retooling a refinery to process sweet crude exclusively involves a series of steps, each with its associated costs. The first step is a thorough assessment of the current infrastructure to identify what modifications are necessary. This includes evaluating distillation units, cracking units, desulfurization facilities, and storage systems. The cost here includes hiring engineering firms for feasibility studies, which can range from hundreds of thousands to millions of dollars depending on the size and complexity of the refinery.

Following the assessment, physical modifications begin. Distillation columns might need resizing or new internals to better handle the lighter components of sweet crude. This can involve significant capital expenditure, often in the tens to hundreds of millions, depending on the extent of the modifications. Cracking units like FCCs or hydrocrackers might need adjustments to optimize for lighter feedstocks, which again involves substantial investment in new catalyst systems, equipment modifications, or even replacement of units. Desulfurization units, less critical for sweet crude, might be repurposed or scaled back, but this still requires investment to either adapt them for other uses or to maintain them in a less intensive operational mode.

Logistical changes, including altering pipelines, storage tanks, and blending facilities, also contribute to the cost. These could range from minor adjustments to significant infrastructure projects, potentially costing millions. Moreover, operational adjustments like retraining staff or recalibrating control systems add to the expense, though these are generally lower compared to physical plant changes.

The total cost for retooling can easily run into the billions for a large refinery, especially considering downtime for construction and potential loss of production during the transition. For instance, retooling to handle lighter U.S. crude could be a 5-year project costing hundreds of millions to billions, reflecting the scale of such undertakings.

Government support?

Regarding government support for these transitions, there are programs and incentives available, though they might not be directly aimed at sweet crude refining but rather at broader energy efficiency, environmental compliance, or innovation in refining technologies:

The Inflation Reduction Act includes provisions for tax credits and rebates for energy efficiency upgrades in industrial facilities, potentially applicable to refining operations. This act offers tax credits for improvements like energy-efficient equipment, which could indirectly benefit refineries transitioning to sweet crude processing due to the different energy demands of sweet versus sour crude refining.

The Department of Energy's (DOE) §48C program provides tax credits for investments in clean energy manufacturing and industrial decarbonization, which could extend to refining if the retooling incorporates technologies that reduce carbon emissions or enhance energy efficiency. This program allocated $4 billion in tax credits, with a portion aimed at critical materials refining, which might include refining technology upgrades.

Additionally, there are general industrial tax credits or grants for research and development that could be leveraged for developing or adapting technologies specific to sweet crude refining. However, these are not explicitly for the purpose of transitioning to sweet crude but rather for broader innovation and environmental benefits.

But there is no direct US government support for retooling either financially directly through subsides or through tax credits or tax rebates.

In fact, there is a tremendous amount of government inertia against retooling. The retooling of refineries to process primarily sweet crude oil involves navigating a complex web of regulatory hurdles, which can significantly influence both the timeline and cost of such projects. At the federal level, one of the primary challenges is compliance with the Clean Air Act and its amendments, which impose stringent standards on emissions from refineries. Any modification to a refinery, particularly one that could potentially increase emissions or alter the type of emissions, requires securing permits under the New Source Review (NSR) program. This means that even if the intent is to reduce overall emissions by switching to lighter, less sulfurous crude, the changes must be evaluated for their impact on air quality. The process of obtaining these permits can be lengthy, involving detailed environmental impact assessments, public comment periods, and potential challenges from environmental groups or local communities.

At the state level, regulations can be even more varied and potentially more restrictive. States like California, for instance, have additional layers of environmental regulations under programs like the California Environmental Quality Act (CEQA), which requires comprehensive environmental impact reports for major modifications. These state regulations can lead to extended review periods, additional local permits, and sometimes, the need for community engagement or negotiation of mitigation measures to offset environmental impacts. Each state might have its own set of rules regarding water usage, waste disposal, and air pollution, all of which need to be addressed with each modification or expansion.

Additionally, there's the issue of safety regulations. The Occupational Safety and Health Administration (OSHA) and the Environmental Protection Agency (EPA) enforce standards related to worker safety and chemical safety management, particularly through the Process Safety Management (PSM) of Highly Hazardous Chemicals standard. Retrofitting a refinery requires ensuring that all new or modified equipment meets these safety standards, which involves extensive documentation, redesign, and potentially new safety protocols, all of which add to the regulatory burden.

The complexity of obtaining permits is compounded by the fact that many refineries are located near sensitive areas like water bodies or residential zones, increasing scrutiny over potential impacts on water quality, noise, and local ecosystems. Refineries must also navigate regulations related to the disposal or recycling of old equipment, which can involve hazardous waste management protocols.

Finally, the regulatory landscape is dynamic, with potential changes in policy or administration leading to shifts in how regulations are interpreted or enforced. This unpredictability can make long-term planning for refinery upgrades challenging. For instance, changes in emission standards or new environmental policies could require further modifications to the retooling plans, leading to additional time and cost for compliance.

In essence, the regulatory hurdles for retooling refineries to sweet crude processing involve navigating a maze of federal, state, and sometimes local laws and regulations, each designed to protect the environment, public health, and worker safety. These hurdles can delay projects, increase costs through compliance measures, and require refineries to maintain a flexible strategy to adapt to evolving regulatory demands.

Retooling pace

Determining the exact percentage of U.S. refineries that have retooled to handle primarily sweet crude oil is challenging due to the nuanced nature of refinery modifications and the lack of comprehensive, public data on such specific changes. However, insights can be gathered from various industry reports, analyses, and news articles.

By 2024, it is clear that a notable shift has occurred within the U.S. refining sector in response to the increased availability of light, sweet crude from shale oil production. According to the U.S. Energy Information Administration (EIA), the number of operable refineries in the U.S. stood at 132 as of January 2024, with a total capacity of about 18.4 million barrels per day.

Industry sources like Reuters and the Oil & Gas Journal have reported that several major refineries have undertaken significant modifications or expansions to better process domestic sweet crude. For example, ExxonMobil completed a major expansion at its Beaumont, Texas refinery in 2023 to handle more light, sweet crude, which suggests a direct adaptation to the U.S. shale boom. Similarly, Marathon Petroleum has adjusted operations at various refineries, including the Galveston Bay facility, to leverage the lighter crude feedstocks.

However, these modifications are often part of broader strategic adjustments rather than exclusive retooling for sweet crude. Many refineries have maintained flexibility to process both sweet and sour crude, reflecting the complexity of market demands and the economic benefits of versatility. The American Fuel & Petrochemical Manufacturers (AFPM) notes that while some refineries have indeed focused on sweet crude, the sector as a whole has been adapting to a mix of crudes due to the fluctuating global supply and demand dynamics.

A rough estimate, based on industry trend analysis and reports from companies like Valero and PBF Energy, suggests that perhaps 20-30% of U.S. refineries have significantly retooled or modified their operations explicitly for sweet crude, focusing on this range because:

Some refineries have made substantial investments to optimize for sweet crude but still retain the capability to process other types.

Others might have adapted incrementally, not fully retooling but making adjustments to handle more sweet crude alongside other types.

This percentage is speculative and based on qualitative assessments from industry news, expert analyses, and the understanding that complete retooling to sweet crude alone is rare due to the need for operational flexibility.

Thus, while a precise percentage is elusive, it's evident that a significant portion, but not the majority, of U.S. refineries have adapted to some degree to handle more sweet crude in response to the shale oil boom.

The imperative to retool

Retooling U.S. refineries to primarily process sweet crude could bring several economic advantages. Firstly, it could significantly reduce the cost of feedstock for these refineries. Sweet crude, particularly from domestic shale resources, is often cheaper to procure than importing sour or heavy crude oils from abroad due to transportation costs, geopolitical risks, and the inherent lower cost of extraction in areas like the Permian Basin or Bakken Formation. This could lead to lower production costs for refined products, potentially allowing U.S. refineries to offer competitive prices in both domestic and international markets.

Secondly, by optimizing for sweet crude, refineries could increase their operational efficiency. Sweet crude requires less complex processing for some products, particularly gasoline, which can lead to higher throughput and yield of high-value products. This efficiency could translate into higher profit margins as less energy and fewer chemicals are needed for refining, reducing operational costs and potential savings at the pump for consumers. Moreover, the simplicity in processing can also mean less downtime for maintenance related to the handling of corrosive, sulfurous elements found in sour crude, potentially leading to more consistent production levels.

Another economic advantage is the potential for increased domestic energy security and independence. By relying less on imports, the U.S. would be less vulnerable to international supply disruptions, price volatility, and geopolitical tensions. This could stabilize energy prices within the country, contributing to economic stability. Additionally, enhancing domestic production and refining capabilities would keep more economic activity within the U.S., fostering job creation in the energy sector and related industries, from drilling to logistics.

Retooling U.S. refineries to primarily process sweet crude could offer direct benefits to consumers, particularly in the form of lower gasoline and fuel prices, if the resulting cost savings are passed on rather than booked as profit. The primary cost advantage comes from the reduced expense of feedstock. Domestic sweet crude from shale regions like the Permian Basin is often cheaper than imported sour or heavy crude due to lower transportation costs and less complex refining processes needed. If refineries pass these savings onto consumers, this could potentially lower the cost at the pump. For instance, if the cost of refining sweet crude reduces the overall production cost by an estimated 10-20% compared to sour or medium crude, and assuming that these savings are fully passed to consumers, this might translate to a reduction in gasoline prices by around $0.20 to $0.40 per gallon, considering that crude oil costs make up roughly 55-60% of the retail gasoline price according to the U.S. Energy Information Administration.

")

In addition to price benefits, retooling could stimulate job creation in several ways. Firstly, the retooling process itself requires skilled labor for engineering, construction, and installation of new or modified equipment. This could lead to a temporary but significant increase in employment in the regions where refineries are located. For example, if a major refinery invests in a $500 million retooling project, this could directly create hundreds of jobs in construction, engineering, and project management over the span of the project, which might last several years.

Beyond the construction phase, retooling could lead to sustained job growth in several aspects:

Operational Jobs: Once retooled, refineries might operate at higher efficiency or capacity, potentially necessitating more workers for operations, maintenance, and logistics. The need to maintain new equipment or manage increased throughput could lead to permanent job creation in these areas.

Supply Chain: An increased focus on domestic crude would likely bolster the upstream sector (oil extraction) and midstream (transportation and storage), creating jobs in drilling, pipeline construction, and transportation sectors. As refineries increase their demand for more local crude, there would be a ripple effect, boosting employment in these supporting industries.

Research and Development: Enhanced capabilities to process sweet crude might encourage investment in R&D to further optimize refining processes, leading to jobs in research, technology development, and innovation within the energy sector.

Economic Ripple Effect: Lower fuel prices could stimulate consumer spending, potentially leading to job growth in other sectors of the economy as well. With more disposable income, consumers might spend more on goods and services, indirectly creating jobs in retail, hospitality, and manufacturing.

In summary, if refineries choose to pass on the savings from retooling to consumers, this could result in a noticeable decrease in fuel prices at the pump, potentially saving consumers money on each fill-up. Concurrently, the process and aftermath of retooling could lead to both short-term and long-term job creation, bolstering local and national economies through direct employment in the refining sector and through the broader economic benefits of lower energy costs.

Trump and refineries

In recent announcements incoming President Trump has verified that his approach to energy policy will be characterized by a dual focus on addressing trade imbalances and achieving "energy dominance," a term that went beyond the more conventional goal of energy independence. Under this theory of energy policy and administration, "energy dominance" is not only about producing enough energy to meet domestic needs but also about leveraging the U.S.'s energy resources to influence global markets, bolster the economy, and strengthen geopolitical standing. This will likely include promoting increased exports of U.S. energy products, particularly oil and natural gas and petroleum refinery products, to reduce trade deficits with countries like China and to counterbalance the power of OPEC in the international arena. The administration aims to roll back regulations perceived as hindering energy production, such as those on drilling in federal lands and waters, and previously withdrew from international agreements like the Paris Climate Accord, which it viewed as constraints on U.S. energy sector growth.

To achieve "energy dominance," the Trump administration will likely emphasize policies that would increase domestic production, streamline regulatory processes, and encourage exports. In his previous administration, this was evident in actions like approving the Keystone XL and Dakota Access pipelines, expanding LNG export capabilities, and promoting the idea that U.S. energy could be a strategic asset in international diplomacy. This strategy aimed at transforming the U.S. into a major energy supplier on the world stage, thereby using its energy resources to negotiate trade agreements, secure economic advantages, and ensure national security.

However, the concept of "complete and total US energy independence," where the U.S. would not import any foreign crude oil, presents a more complex challenge, particularly in light of the existing refining infrastructure. Much of the U.S. refining capacity was historically built to process a variety of crude types, including heavy, sour crude from imports, especially from the Middle East and Venezuela. Achieving true energy independence in this sense would necessitate a significant retooling of refineries to focus solely on the type of crude predominantly produced domestically, which is light, sweet crude from shale formations.

Retooling to process only domestic sweet crude would involve substantial investment in modifying distillation columns, reducing or repurposing desulfurization units, and optimizing cracking units for lighter hydrocarbons. This transformation would allow refineries to operate more efficiently with domestic crude, potentially eliminating the need to import foreign crude.

Without government support, we will not achieve true energy independence or energy dominance

Without subsidies, tax credits, or tax rebates, it is highly unlikely that all U.S. refineries would choose to retool to process primarily sweet crude oil. The primary reason is the substantial financial investment required for such retooling. As such, foreign crude importing will continue. Modifying a refinery to handle different types of crude involves significant capital expenditure for new or adapted equipment, engineering studies, construction, and operational downtime, which could run into hundreds of millions or even billions of dollars per facility. Refineries operate on tight margins, driven by the cost of crude oil, refining costs, and the fluctuating prices of refined products. Without financial incentives, the economic justification for such an overhaul might not be compelling enough, especially considering the risks and uncertainties involved, like potential shifts in crude oil supply, demand for refined products, or changes in environmental regulations.

To encourage retooling, the following types of subsidies, tax credits, or tax rebates could be considered:

Investment Tax Credits: These could offer a percentage of the capital expenditure back to refineries as a tax credit. This would directly reduce the net cost of retooling, making the financial decision more attractive. For instance, credits similar to those in the Inflation Reduction Act for clean energy investments could be adapted for refining upgrades that enhance efficiency or reduce emissions. This is the type of solution that the US Chips Act has used for semiconductors.

Production Tax Credits: Credits based on the volume of refined products from domestic crude could incentivize refineries to switch to processing more local sweet crude, especially if the credit structure rewards cleaner or more efficient production processes.

Accelerated Depreciation: Allowing faster write-offs for new equipment or modifications could improve cash flow for refineries, making the upfront cost of retooling less daunting. This would be particularly beneficial for the significant investments in machinery and technology needed for sweet crude processing.

Grants or Low-Interest Loans: Direct financial support or access to cheaper capital could offset the initial cost barrier. Programs like the DOE's §48C tax credit, which supports advanced energy projects, could be expanded to include refining infrastructure upgrades.

Environmental Compliance Credits: Given the potential environmental benefits of processing lighter, sweeter crude (like reduced sulfur emissions), credits or rebates for achieving specific environmental performance benchmarks could be a motivator.

Energy Efficiency Rebates: Incentives for adopting technologies or processes that reduce energy consumption in refining could be part of broader energy efficiency initiatives, indirectly supporting the shift towards sweet crude processing.

However, the availability and structure of these incentives would need to balance between encouraging necessary industry transitions while managing public fiscal responsibility. Without these financial mechanisms, the economic case for retooling without subsidies or tax benefits would be weak, leading to a scenario where only refineries with a strategic advantage or those compelled by market forces might undertake such costly projects.

Conclusion:

The United States' continued reliance on oil imports, despite its position as a leading crude oil producer, underscores the intricate balance between production, refining capabilities, and market dynamics. The historical configuration of U.S. refineries, optimized for processing sour and medium crude oils, remains a key factor driving the need for foreign oil imports. At the same time, the shale revolution has shifted the country's oil production landscape, providing an abundance of light, sweet crude that is not fully compatible with many existing refinery setups.

Efforts to adapt, such as retooling refineries to process primarily sweet crude, face significant financial and regulatory hurdles, further complicating the transition. Without substantial government incentives or subsidies, achieving complete energy independence or dominance—where imports become unnecessary—remains an unlikely scenario. However, the U.S. has leveraged its advanced refining infrastructure and increased production to solidify its role as a major player in global energy markets, both as a leading exporter of refined products and a net exporter of crude oil.

While challenges remain, the adaptability of the U.S. refining sector and the strategic management of its resources will continue to shape its position in the global energy landscape. Understanding the interplay between refining capabilities, crude oil types, and market demands offers valuable insight into the complexities of achieving true energy security in a dynamic and interconnected world.

Sources:

Statista. (n.d.). Oil refinery capacity in the United States. Retrieved from https://www.statista.com/statistics/265273/oil-refinery-capacity-in-the-united-states/

Statista. (n.d.). Operative oil refineries in the U.S. Retrieved from https://www.statista.com/statistics/1447051/operative-oil-refineries-in-the-us/

American Fuel & Petrochemical Manufacturers (AFPM). (n.d.). Refining capacity 101: What to understand about demanding restarts. Retrieved from https://www.afpm.org/newsroom/blog/refining-capacity-101-what-understand-demanding-restarts

U.S. Energy Information Administration (EIA). (n.d.). U.S. refinery capacity by year. Retrieved from https://www.eia.gov/dnav/pet/pet_pnp_cap1_dcu_nus_a.htm

U.S. Energy Information Administration (EIA). (n.d.). Refinery capacity report. Retrieved from https://www.eia.gov/petroleum/refinerycapacity/

Statista. (n.d.). Countries with the largest oil refinery capacity. Retrieved from https://www.statista.com/statistics/273579/countries-with-the-largest-oil-refinery-capacity/

Statista. (n.d.). Forecast for petroleum refinery end-use market output in the United States. Retrieved from https://www.statista.com/statistics/407793/forecast-for-petroleum-refinery-end-use-market-output-in-the-united-states/

Reuters. (2020, June 22). U.S. crude oil refining capacity nears 19 million bpd: U.S. EIA. Retrieved from https://www.reuters.com/article/us-refineries-capacity/u-s-crude-oil-refining-capacity-nears-19-million-bpd-u-s-eia-idUSKBN23W09T/

U.S. Energy Information Administration (EIA). (n.d.). Refining crude oil: Refinery rankings. Retrieved from https://www.eia.gov/energyexplained/oil-and-petroleum-products/refining-crude-oil-refinery-rankings.php

U.S. Energy Information Administration (EIA). (n.d.). U.S. operable refineries and utilization. Retrieved from https://www.eia.gov/dnav/pet/pet_pnp_unc_dcu_nus_m.htm

Observatory of Economic Complexity (OEC). (n.d.). Refined petroleum. Retrieved from https://oec.world/en/profile/hs/refined-petroleum

U.S. International Trade Commission (USITC). (2014). Petroleum products: Trends in U.S. production and trade. Retrieved from https://www.usitc.gov/research_and_analysis/documents/foreso_petroleum_products-12-1-14_final_0.pdf

World's Top Exports. (n.d.). Refined oil exports by country. Retrieved from https://www.worldstopexports.com/refined-oil-exports-by-country/

Statista. (n.d.). Refined oil products production by country worldwide. Retrieved from https://www.statista.com/statistics/1445672/refined-oil-products-production-by-country-worldwide/

Observatory of Economic Complexity (OEC). (n.d.). Refined petroleum: U.S. export profile. Retrieved from https://oec.world/en/profile/bilateral-product/refined-petroleum/reporter/usa

USAFacts. (n.d.). Is the U.S. a bigger oil importer or exporter? Retrieved from https://usafacts.org/articles/is-the-us-a-bigger-oil-importer-or-exporter/

Strauss Center. (n.d.). The U.S. shale revolution. Retrieved from https://www.strausscenter.org/energy-and-security-project/the-u-s-shale-revolution/

Trading Economics. (n.d.). United States crude oil production. Retrieved from https://tradingeconomics.com/united-states/crude-oil-production

MacroTrends. (n.d.). U.S. crude oil production historical chart. Retrieved from https://www.macrotrends.net/2562/us-crude-oil-production-historical-chart

U.S. Energy Information Administration (EIA). (n.d.). U.S. refinery throughput and capacity. Retrieved from https://www.eia.gov/todayinenergy/detail.php?id=61545

Council on Foreign Relations (CFR). (n.d.). Shale gas and tight oil boom. Retrieved from https://www.cfr.org/report/shale-gas-and-tight-oil-boom

American Fuel & Petrochemical Manufacturers (AFPM). (n.d.). Refining capacity 101: What to understand about demanding restarts. Retrieved from https://www.afpm.org/newsroom/blog/refining-capacity-101-what-understand-demanding-restarts

Springer. (n.d.). Refining strategies for crude oil. Retrieved from https://link.springer.com/chapter/10.1007/978-3-319-49347-3_31

American Petroleum Institute (API). (n.d.). Refinery processes: How a refinery works. Retrieved from https://www.api.org/oil-and-natural-gas/wells-to-consumer/fuels-and-refining/refineries/how-refinery-works/refinery-processes

RBN Energy. (n.d.). Comin’ to America: Major changes in crude oil imports as refineries’ needs shift. Retrieved from https://rbnenergy.com/comin-to-america-major-changes-in-crude-oil-imports-as-refineries-needs-shift

Energy Policy Institute at the University of Chicago (EPIC). (n.d.). Why do we import Russian and other foreign oil when we have a lot of it in the U.S.? Retrieved from https://epic.uchicago.edu/news/why-do-we-import-russian-and-other-foreign-oil-when-we-have-a-lot-of-it-in-the-u-s/

Oil & Gas Journal (OGJ). (n.d.). Survey finds U.S. refiners capable of processing more light sweet crude. Retrieved from https://www.ogj.com/refining-processing/refining/operations/article/17244906/survey-finds-us-refiners-capable-of-processing-more-light-sweet-crude

American Fuel & Petrochemical Manufacturers (AFPM). (n.d.). U.S. refiners clean trade: Their own exports soar. Retrieved from https://www.afpm.org/newsroom/blog/us-refiners-clean-trade-their-own-exports-soar

U.S. Energy Information Administration (EIA). (n.d.). Evolving refining challenges. Retrieved from https://www.eia.gov/todayinenergy/detail.php?id=54199

Reuters. (2018, April 25). Skinny and sweet: U.S. refiner earnings depend on the oil diet. Retrieved from https://www.reuters.com/article/us-usa-oil-refineries/skinny-and-sweet-u-s-refiner-earnings-depend-on-the-oil-diet-idUSKBN1HX0H8/

Reuters. (2023, January 18). Heavy slate: U.S. oil refinery overhauls crimp fuel output. Retrieved from https://www.reuters.com/business/energy/heavy-slate-us-oil-refinery-overhauls-crimp-fuel-output-2023-01-18/

American Fuel & Petrochemical Manufacturers (AFPM). (n.d.). Refinery earnings: Here’s why. Retrieved from https://www.afpm.org/newsroom/blog/refinery-earnings-are-why

Berman, A. (n.d.). Refinery crisis. Retrieved from https://www.artberman.com/blog/refinery-crisis/

Bain & Company. (n.d.). Retooling for the new cost imperative. Retrieved from https://www.bain.com/insights/retooling-for-the-new-cost-imperative/

House Representative Davids. (n.d.). Davids calls to increase refining capacity to lower gas prices. Retrieved from https://davids.house.gov/media/press-releases/davids-calls-increase-refining-capacity-lower-gas-prices

American Fuel & Petrochemical Manufacturers (AFPM). (n.d.). What do refineries have to do with the price and availability of gas? Retrieved from https://www.afpm.org/newsroom/blog/what-do-refineries-have-do-price-and-availability-gas

American Fuel & Petrochemical Manufacturers (AFPM). (n.d.). Supporting millions of jobs and contributing billions: Understanding the economic impact of U.S. refineries. Retrieved from https://www.afpm.org/newsroom/blog/supporting-millions-jobs-and-contributing-billions-understanding-economic-impact-us