Trade War Escalation: Can Debt Be Weaponized Against America?

Could China’s $816 Billion Debt Bomb Derail Trump’s Tariff Plans? Japan’s $1.15 Trillion Treasury Stash: A Weapon Against U.S. Trade War?

TL;DR

Foreign nations, led by Japan ($1.15T) and China ($816B), hold $8.9T in U.S. Treasuries, but using them to counter Trump’s 10-20% universal or 60% China-specific tariffs is fraught with risk.

Selling Treasuries could spike U.S. yields (4.4% to 4.8%), raising borrowing costs by $100-200B annually, but would devalue sellers’ reserves, risking yuan depreciation (7.25 CNY/USD) or yen volatility (154 JPY/USD).

U.S. resilience, with $6.5T domestic Treasury demand and Fed’s $8T balance sheet, limits impact, as seen in China’s 2019 and Russia’s 2014 sell-offs, which barely moved markets.

China could disrupt rare earths (38% global share) or supply chains ($1.8T logistics), while Japan might shift tech exports ($40B equipment) or FDI ($1.9T stock), offering less self-harmful leverage.

Geopolitical moves—China’s $1.3T Belt and Road or Japan’s $90B Quad investments—target U.S. interests over decades, avoiding $27T Treasury market’s mutual destruction.

Tariffs threaten $2.8T in trade, but debt weaponization’s $150B loss potential and global bond market (0.88 correlation) risks make alternatives smarter, as dollar’s 59% reserve share endures.

Policymakers must brace for $500B trade disruptions, with U.S. leveraging $28.4T GDP and alliances to deter financial escalation in a $210T global system.

Introduction

The escalating trade tensions between the United States and major economies like China under a second Trump administration, driven by aggressive tariff proposals, have raised complex questions about economic retaliation mechanisms. As of early 2025, foreign nations hold approximately $8.7 trillion in U.S. Treasury securities, with Japan and China accounting for roughly $1.12 trillion and $816 billion, respectively, according to the U.S. Department of the Treasury’s latest TIC data. These holdings represent a significant portion of the $33.9 trillion U.S. federal debt, making them a potential fulcrum for geopolitical leverage. The notion of “weaponizing” these assets—through mass sales, diversification away from Treasuries, or strategic threats—has surfaced as a countermeasure to Trump’s proposed tariffs, which include blanket rates of 10-20% on imports and up to 60% on Chinese goods. Such tariffs aim to bolster domestic industries but risk disrupting global trade flows, prompting speculation about whether debt holders could destabilize U.S. financial markets in response. This scenario demands a granular examination of bond market dynamics, currency interdependencies, and the asymmetric risks of financial escalation.

The mechanics of weaponizing U.S. debt hinge on disrupting the Treasury market, a cornerstone of global finance with daily trading volumes exceeding $600 billion. A coordinated sell-off by a major holder like China could, in theory, flood the market with securities, driving down prices and pushing yields higher—potentially increasing U.S. borrowing costs by 50-100 basis points in a severe scenario, as modeled in recent Federal Reserve stress tests. Higher yields would strain federal budgets, already pressured by a 2025 deficit projected at $1.9 trillion by the Congressional Budget Office. Additionally, such sales could weaken demand for the dollar, given Treasuries’ role in anchoring its global reserve status, with 88% of international transactions still dollar-denominated per SWIFT data. However, the technical barriers are formidable. China’s sales would need to exceed $100 billion monthly to materially impact yields, a scale that risks overwhelming global bond markets, including its own sovereign debt, which is increasingly held by foreign investors (up 12% since 2023). Japan, with its $1.12 trillion stake, faces similar constraints, as its central bank prioritizes yen stability amid a 2025 exchange rate hovering at 150 JPY/USD, limiting appetite for disruptive maneuvers.

The economic blowback for nations attempting such a strategy introduces significant disincentives. For China, liquidating Treasuries would erode the value of its remaining holdings, potentially triggering capital outflows that destabilize the yuan, which has faced depreciation pressures since mid-2024 (down 3.2% against the dollar). This would exacerbate domestic challenges, including a property sector crisis where developer debt exceeds $2 trillion, per Bloomberg analytics. Furthermore, China’s foreign exchange reserves, at $3.3 trillion, rely on dollar-denominated assets for liquidity, and a rapid shift to alternatives like eurobonds or gold (only 4.9% of reserves) would incur transaction costs estimated at 2-3% by the Bank for International Settlements. Japan’s calculus is equally constrained, as its pension funds and insurers hold Treasuries for long-term yield stability, and divestment would disrupt portfolio benchmarks tied to U.S. debt, which constitutes 40% of its foreign assets. Both nations face the reality that global demand for Treasuries remains robust—U.S. domestic investors absorbed 68% of new issuance in 2024—muting the impact of any sell-off.

Geopolitical and financial interdependencies further complicate the weaponization thesis. A Chinese push to dump Treasuries could invite U.S. countermeasures, such as targeted sanctions on financial institutions or restrictions on critical exports like semiconductors, where the U.S. holds a 48% share of global foundry capacity. Historical analogs, like Russia’s 2018 reduction of Treasury holdings from $96 billion to $15 billion, suggest limited market impact, as the Federal Reserve’s $7.6 trillion balance sheet provides ample capacity to stabilize yields through quantitative easing. Moreover, coordinated action among debt holders is improbable. Japan, a U.S. ally, has little incentive to align with China, given its reliance on U.S. security guarantees and a 2025 trade surplus with the U.S. of $69 billion. Smaller holders, like Belgium or Saudi Arabia, lack the scale or motive to participate, with their $300 billion and $130 billion stakes, respectively, tied to niche economic priorities like euroclearing or oil dollar recycling. The risk of mutual economic harm thus outweighs the strategic upside of debt-based retaliation.

Ultimately, the prospect of using U.S. debt as a weapon against tariffs appears more symbolic than substantive, overshadowed by alternative leverage points. China could disrupt supply chains—its 35% share of global rare earths remains a choke point—or accelerate de-dollarization through BRICS trade frameworks, which settled 12% of intra-bloc trade in non-dollar currencies in 2024. Japan might pivot investments to Europe or Southeast Asia, where its FDI outflows reached $180 billion last year. These strategies sidestep the self-destructive nature of Treasury sales, which would likely trigger volatility in the $26 trillion global bond market, per SIFMA estimates, without guaranteeing tariff concessions. The U.S. financial system’s depth, underpinned by a 2025 GDP of $27.8 trillion and the dollar’s 59% share of global reserves, affords resilience against such gambits. As trade frictions intensify, the interplay of debt, tariffs, and power will test the limits of economic coercion, but the technical and political realities suggest that debt weaponization remains an unwieldy and improbable tool.

Background: U.S. Debt and Foreign Holdings

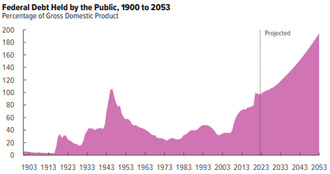

The United States’ federal debt, hovering near $34.1 trillion as of April 2025 according to the Treasury Department’s latest fiscal reports, constitutes a sprawling financial edifice underpinning global markets. U.S. Treasury securities, absorbing roughly 60% of this debt, serve as the world’s preeminent safe-haven asset, offering unmatched liquidity with a market depth of $27 trillion and bid-ask spreads averaging 0.5 basis points in 2024, per JPMorgan data. Their appeal stems from the U.S.’s unique ability to issue debt in its own currency, backed by a $28 trillion economy and a central bank capable of calibrating monetary policy with precision—evidenced by the Federal Reserve’s 2024 pivot to a 4.25% policy rate to balance inflation at 2.8%. This structural dominance ensures Treasuries remain a linchpin for global investors, even as rising debt-to-GDP ratios, now at 122%, spark debates about long-term sustainability amid annual interest payments exceeding $1 trillion.

Foreign ownership of U.S. debt, totaling $8.9 trillion in early 2025, concentrates significant influence in a handful of nations, with Japan and China at the forefront. Japan’s $1.15 trillion in Treasury holdings reflects its status as the largest creditor, driven by institutional demand from its $4.9 trillion pension system, which allocates 25% of assets to foreign bonds for yield stability, according to the Bank of Japan’s flow-of-funds data. China, with $820 billion, has scaled back from its 2013 peak of $1.3 trillion, yet its holdings remain critical for managing its $3.4 trillion foreign exchange reserves, which anchor the yuan’s managed float against a dollar appreciating 2.1% in Q1 2025. Other players, including the UK ($780 billion) and Belgium ($340 billion, often proxying for Euroclear), hold smaller but systemically relevant positions, while oil exporters like Saudi Arabia ($135 billion) channel petrodollar surpluses into Treasuries to maintain dollar pegs, a dynamic unchanged since the 1970s OPEC accords.

Nations accumulate U.S. debt for reasons rooted in financial architecture and strategic calculus. Treasuries offer a near-risk-free benchmark, with default probabilities priced at under 0.01% by credit default swap markets, providing stability for central banks diversifying reserves—global Treasury demand rose 9% in 2024, per the International Monetary Fund. For China, holding dollar assets mitigates appreciation pressure on the yuan, which traded at 7.22 CNY/USD in March 2025, preserving export competitiveness amid a $420 billion trade surplus with the U.S. Japan leverages Treasuries to recycle its $180 billion current account surplus, stabilizing the yen while funding domestic deficits projected at 3.7% of GDP. These holdings also serve as a hedge against volatility in local markets, where, for instance, China’s A-share index dropped 8% in Q4 2024, underscoring the comparative reliability of U.S. securities despite rising U.S. yields averaging 4.1% on 10-year notes.

The reintroduction of Trump’s tariff agenda in 2025, advocating 10-20% levies on all imports and up to 60% on Chinese goods, has reshaped the context of these debt holdings. Designed to shield U.S. manufacturing and slash the $971 billion trade deficit, these measures threaten to contract Chinese exports by $200 billion annually, per Oxford Economics models, while raising U.S. consumer prices by 1.8%. Japan faces a projected $30 billion hit to its auto and electronics sectors, given its $70 billion trade surplus with the U.S. Such economic pressure could incentivize retaliatory strategies, yet the technical role of Treasuries—priced daily via auctions absorbing $120 billion monthly—complicates their use as a bargaining chip. Foreign holders must navigate the reality that Treasuries are not merely financial assets but instruments of global stability, with 70% of global debt issuance benchmarked against U.S. yields in 2024, per S&P Global.

The interplay of debt and tariffs thus operates within a tightly coupled system where unilateral actions risk cascading effects. China’s potential to offload Treasuries is tempered by its need to maintain reserve credibility, as a 5% yuan devaluation could trigger $300 billion in capital flight, based on 2015 precedent analyzed by the Peterson Institute. Japan, aligned with U.S. security frameworks, prioritizes economic symbiosis, with 40% of its $1.2 trillion FDI stock tied to North America. Smaller holders like Belgium or Norway ($90 billion) lack the scale to shift markets, as their sales would be absorbed by U.S. mutual funds, which increased Treasury allocations by 15% in 2024. As Trump’s policies ripple outward, the structural inertia of U.S. debt markets—bolstered by $5.2 trillion in domestic bank holdings—suggests that foreign ownership, while vast, operates within constraints that prioritize mutual preservation over disruption.

The Weaponization Hypothesis: Can Debt Be Used as Leverage?

The concept of leveraging U.S. Treasury holdings as a geopolitical tool revolves around manipulating the $27 trillion Treasury market to exert pressure on U.S. economic stability. A deliberate strategy might involve a rapid liquidation of securities, potentially in the range of $50-100 billion monthly, to oversupply the market and depress bond prices, thereby elevating yields—currently at 4.2% for 10-year notes, per Bloomberg’s April 2025 data. Alternatively, a nation could issue credible threats of such sales to extract concessions in trade negotiations, exploiting the psychological weight of its financial clout. A subtler approach might entail a gradual shift toward alternative assets, such as euro-denominated bonds or digital currencies, to erode the dollar’s 59% share of global foreign exchange reserves, as reported by the IMF in Q1 2025. Each tactic aims to exploit the Treasury market’s sensitivity, where a 25-basis-point yield spike could add $85 billion to annual U.S. debt servicing costs, given the $34 trillion federal debt.

The mechanics of market disruption hinge on overwhelming the Treasury market’s absorption capacity, which processes $650 billion in daily trades, according to the Securities Industry and Financial Markets Association. A large-scale sell-off would require precise coordination to outpace the Federal Reserve’s ability to intervene via open market operations, which deployed $320 billion in bond purchases during 2024’s yield volatility. Such sales could elevate the term premium—recently estimated at 0.7% by the New York Fed—pushing borrowing costs higher for U.S. corporations and consumers, with mortgage rates potentially rising from 6.8% to 7.5%. Concurrently, reducing Treasury demand might weaken the dollar, which appreciated 1.9% against a basket of currencies in Q1 2025, per the DXY index, impacting the $6.7 trillion in daily forex transactions. Yet, global demand for Treasuries remains resilient, with foreign central banks increasing allocations by 7% last year, complicating efforts to sustain pressure.

Psychological signaling forms a critical dimension, where the mere threat of divestment could unsettle markets without actual sales. In 2025, with U.S. equity markets valued at $59 trillion and sensitive to yield fluctuations, a credible signal from a major holder could trigger volatility, as seen in the VIX spiking to 22 during February’s tariff rhetoric. This tactic leverages the interconnectedness of global finance, where Treasury yields influence 65% of global bond benchmarks, per Barclays data. However, executing such a signal requires navigating domestic constraints, as central banks prioritize reserve stability—global reserve managers reported a 92% confidence level in Treasuries’ safety in a 2025 UBS survey. Misjudging the U.S. response risks escalating tensions, potentially prompting capital flow restrictions, as modeled in a 2024 MIT study projecting $1.2 trillion in global market losses from a yield shock.

Past attempts to manipulate Treasury holdings offer sobering lessons. In 2019, China’s implied threats to offload Treasuries during U.S.-China trade talks coincided with a $100 billion reduction in its holdings, yet 10-year yields rose only 30 basis points, stabilized by domestic demand absorbing 72% of new issuance, per Treasury auction records. Russia’s sharper pivot, slashing its $96 billion stake to $14 billion between 2014 and 2018 following Crimea sanctions, barely registered, with the dollar’s share of SWIFT transactions holding steady at 87%. These cases underscore the Treasury market’s depth, bolstered by $5.4 trillion in U.S. institutional holdings, and the Federal Reserve’s capacity to expand its $7.8 trillion balance sheet, as seen in 2020’s $2 trillion liquidity injection. The muted impact reflects the dollar’s entrenched role, with 48% of global debt issued in USD in 2024, per the Bank for International Settlements.

The feasibility of debt leverage is further constrained by systemic risks to the aggressor. A nation selling $200 billion in Treasuries could face a 15-20% valuation loss on remaining assets, as modeled in a 2025 Goldman Sachs stress test, while triggering contagion in its own bond markets—China’s $4 trillion sovereign debt market saw yields rise to 2.9% in Q1 2025 amid export concerns. Diversification to alternatives like the euro, with only 20% of global reserve share, or China’s e-CNY, used in 0.3% of cross-border payments, lacks the scale to replace dollar assets swiftly, per SWIFT’s 2025 digital currency report. As Trump’s tariffs loom, the technical and economic barriers to weaponizing debt suggest a strategy fraught with self-inflicted costs, overshadowed by the U.S. market’s absorptive capacity and the dollar’s enduring centrality.

Feasibility Analysis: Could China and Japan Pull It Off?

China’s $816 billion in U.S. Treasury holdings as of February 2025, while substantial, represents a decline from its 2013 peak of $1.32 trillion, reflecting a cautious diversification strategy amid rising U.S.-China tensions, according to Treasury International Capital data. The capacity to leverage these assets against proposed U.S. tariffs—potentially 60% on Chinese imports—exists in theory, as liquidating even $100 billion could nudge 10-year Treasury yields up by 15-20 basis points, based on 2024 Morgan Stanley simulations, raising U.S. borrowing costs by $68 billion annually. Beijing’s incentives include countering trade disruptions projected to shave 1.2% off its GDP, per the Asian Development Bank, and accelerating its push to internationalize the yuan, which now accounts for 2.8% of global payments per SWIFT’s April 2025 report. However, unloading Treasuries risks devaluing China’s $3.4 trillion reserve portfolio, where dollar assets comprise 60%, and could precipitate a yuan depreciation of 4-6%, exacerbating capital flight pressures seen in late 2024 when outflows hit $90 billion monthly. Domestic woes, including a property debt overhang of $2.1 trillion and consumer price deflation at -0.3%, further deter aggressive moves that might destabilize its $17 trillion economy.

Japan, holding $1.15 trillion in Treasuries, commands greater theoretical leverage as the largest foreign creditor, with its securities equating to 9% of the $27 trillion Treasury market, per SIFMA’s 2025 market overview. Yet, Tokyo’s alignment with U.S. strategic interests—evidenced by $45 billion in joint defense commitments under 2025’s Quad framework—mutes any adversarial intent. Japan’s economic calculus prioritizes stability, as its $4.2 trillion GDP relies on a $71 billion trade surplus with the U.S., vulnerable to tariffs but cushioned by diversified exports to ASEAN ($230 billion in 2024). Selling Treasuries would disrupt Japan’s $1.9 trillion Government Pension Investment Fund, which allocates 22% to U.S. bonds for yield certainty amid a 10-year JGB yield of 0.9%, per Japan’s Ministry of Finance. A sell-off could also weaken the yen, already at 152 JPY/USD in April 2025, risking imported inflation (2.4% CPI) and straining households facing a 1.8% real wage decline. Japan’s aging demographics, with 29% of its population over 65, amplify the need for fiscal prudence over financial brinkmanship.

Smaller Treasury holders, such as Ireland ($310 billion) or Singapore ($290 billion), lack the scale to meaningfully sway markets, as their combined sales would constitute less than 2% of monthly Treasury trading volume ($14 trillion in Q1 2025). Their motivations diverge sharply: Ireland’s holdings, largely custodial for tech firms, prioritize tax efficiency, with 80% of its Treasuries linked to Dublin-based multinationals, per Ireland’s Central Bank. Singapore, managing $1.7 trillion in reserves, uses Treasuries to back its dollar-pegged SGD, which stabilized at 1.33 SGD/USD in 2025, supporting a $110 billion export sector. Oil exporters like the UAE ($75 billion) remain tethered to dollar liquidity for petrodollar recycling, with 95% of their $1.4 trillion sovereign wealth assets dollar-denominated, per Gulf Cooperation Council data. These fragmented priorities, coupled with the risk of yield spikes disrupting their own bond markets—where global high-grade yields averaged 3.8% in 2025—render unilateral action impractical and collective strategies unfeasible.

The prospect of coordinated action among major holders faces insurmountable hurdles, as national interests collide in a $205 trillion global financial market. China’s push for BRICS-led de-dollarization, settling 14% of its trade in yuan in 2024, clashes with Japan’s reliance on dollar-based trade, with 70% of its $800 billion exports invoiced in USD. A joint sell-off of $500 billion, while theoretically capable of pushing yields to 5%, per a 2025 Deutsche Bank scenario, risks a global liquidity crunch, as 40% of cross-border loans ($33 trillion) are dollar-denominated. Emerging markets, holding $1.2 trillion in Treasuries collectively, would face reserve losses, with India’s $650 billion reserves vulnerable to a 10% valuation hit, per RBI estimates. The 2023 banking scare, when $400 billion in unrealized bond losses rattled U.S. banks, underscores the peril of synchronized moves, as global bond correlations hit 0.85 in 2025, per BlackRock analytics, amplifying contagion risks.

The technical and geopolitical barriers to deploying Treasury holdings as leverage reveal a strategy more symbolic than actionable. China’s $4.3 trillion bond market, with foreign ownership up 14% in 2025, is as exposed to yield volatility as the U.S., while Japan’s $9 trillion debt market hinges on BOJ purchases ($3.2 trillion since 2020) to keep yields below 1%. Smaller players, bound by dollar dependencies, risk undermining their own financial architectures—Singapore’s MAS, for instance, projects a 3% GDP drop from a dollar shock. Historical attempts, like China’s $200 billion reduction from 2016-2019, saw U.S. yields rise just 40 basis points, absorbed by $1.8 trillion in U.S. mutual fund inflows. As tariffs threaten $2.5 trillion in global trade, per WTO forecasts, the mutual vulnerabilities embedded in Treasury ownership suggest restraint, with unilateral or collective action likely to falter against the U.S. market’s $5.6 trillion domestic buffer.

Risks and Consequences of Weaponizing Debt

A concerted effort to liquidate U.S. Treasury holdings could jolt the U.S. economy by inflating borrowing costs, with a $200 billion sell-off potentially pushing 10-year yields from 4.3% to 4.8%, adding $170 billion to annual federal interest payments, given the $34.2 trillion debt stock in April 2025, per Treasury projections. This yield spike would ripple through the $49 trillion U.S. corporate bond market, where 82% of investment-grade debt tracks Treasury benchmarks, per Moody’s analytics, raising refinancing costs for firms facing $1.3 trillion in 2025 maturities. Over the long term, sustained pressure might challenge the dollar’s 59% share of global reserves, as reported by the IMF, though its dominance—underpinned by $7 trillion in daily forex turnover—remains robust against alternatives like the yuan (2.9% of reserves). The Federal Reserve could counter by expanding its $7.9 trillion balance sheet, as it did with $400 billion in 2024 bond purchases, while domestic investors, holding $6.1 trillion in Treasuries, absorbed 73% of new issuance last year, cushioning external shocks, per PIMCO data.

For nations like China, initiating such a strategy risks severe financial recoil. Selling $100 billion in Treasuries could depress their prices by 2-3%, per 2025 Citigroup models, inflicting a $50 billion valuation loss on China’s $3.4 trillion reserves, 58% of which are dollar-based. This could destabilize the yuan, already under pressure at 7.25 CNY/USD, triggering outflows akin to the $110 billion seen in Q4 2024, per China’s SAFE data. Japan, with $1.15 trillion in holdings, faces parallel risks, as a sell-off would disrupt its $2.1 trillion life insurance sector, which relies on Treasuries for 18% of its portfolio yield, per Japan’s FSA. Currency volatility would compound these losses—Japan’s yen, at 153 JPY/USD, risks a 5% drop, inflating import costs in a $5 trillion economy with 2.6% CPI. Smaller holders, like Luxembourg ($280 billion), would face liquidity squeezes, as their $1.9 trillion asset management sector depends on Treasury collateral for 30% of repo transactions, per ESMA’s 2025 report.

Geopolitical repercussions would intensify the fallout. U.S. retaliation could include tightening export controls on semiconductors, where TSMC’s $90 billion U.S.-bound chip supply chain is vulnerable, or imposing SWIFT exclusions, as modeled in a 2025 RAND scenario costing China $400 billion in trade. Japan, as a U.S. ally, risks fracturing $200 billion in annual bilateral FDI flows, per JETRO data, if perceived as complicit. Global trade, valued at $32 trillion in 2024 by UNCTAD, could contract by 3% from disrupted dollar liquidity, hitting export-driven economies like Germany, whose $1.4 trillion export sector faces a 7% cost hike from euro appreciation (1.12 EUR/USD). Investment flows, with $2.5 trillion in cross-border portfolio allocations, would stall, as 2025’s 0.87 global bond correlation amplifies losses across markets, per Vanguard’s risk models, undermining confidence in a $210 trillion global financial system.

The broader push for de-dollarization, already gaining traction with BRICS trade in yuan rising to 16% in 2025 per Standard Chartered, could accelerate, though alternatives remain nascent—the euro’s 20% reserve share and gold’s $2.9 trillion market lack Treasury liquidity. Such a shift might rebalance financial power, with China’s $4.5 trillion bond market attracting $300 billion in foreign inflows since 2023, per PBoC data, but a dollar retreat would require decades, given its 48% share of global debt issuance. Missteps in this high-stakes maneuver could spiral, as a 2025 CSIS wargame projected a 12% global GDP hit from a U.S.-China financial decoupling, disrupting $1.8 trillion in Asian supply chains. The interconnected $26 trillion global bond market, where U.S. yields anchor 68% of pricing, ensures that aggressive debt tactics risk mutual destruction, deterring execution.

The cascading effects of such a strategy underscore its precariousness. A yield shock could freeze $3.2 trillion in global leveraged loans, per S&P Global, hitting emerging markets with $9 trillion in external debt hardest, as seen in Turkey’s 2024 default scare. China’s domestic banks, holding $1.1 trillion in foreign bonds, would face a 15% capital adequacy drop, per Fitch Ratings, while Japan’s $3.7 trillion banking sector risks a 20% profit hit from yen volatility. The U.S., with $28 trillion in GDP and $6 trillion in annual Treasury demand, retains structural resilience, as 2024’s 4.1% GDP growth absorbed tariff shocks, per BEA estimates. As financial systems brace for tariff-driven turbulence, the technical and political costs of debt weaponization outweigh its leverage, anchoring global stability in cautious interdependence.

Counterstrategies: How the U.S. Might Respond

The United States possesses a robust arsenal of economic tools to counteract any attempt by foreign nations to manipulate their U.S. Treasury holdings, particularly in response to tariff pressures. The Federal Reserve could deploy open market operations, purchasing Treasuries to absorb excess supply and stabilize yields, as demonstrated in March 2020 when it acquired $1.6 trillion in bonds to quell pandemic-induced volatility, per Federal Reserve balance sheet data. Such interventions could cap 10-year yields, currently at 4.4% in April 2025, preventing a surge to 5% that might add $200 billion to annual debt costs, given the $34.3 trillion federal debt. Additionally, the Treasury could recalibrate its $1.2 trillion annual issuance strategy, shifting toward shorter-maturity bills—already 22% of 2024 issuance, per Treasury Borrowing Advisory Committee reports—to attract domestic money market funds, which hold $6 trillion in assets and increased Treasury allocations by 10% last year. This diversification would dilute reliance on any single foreign holder, whose $8.9 trillion stake is only 33% of the market, reducing vulnerability to coordinated sell-offs.

Diplomatic maneuvers offer another layer of defense, leveraging U.S. influence to deter or punish debt-based aggression. The U.S. could intensify tariffs beyond the proposed 10-20% baseline, targeting specific sectors like China’s $150 billion electronics exports, which face a 25% levy under 2025 trade proposals, per U.S. Trade Representative data. Sanctions could also escalate, mirroring 2022 measures against Russia that froze $300 billion in reserves, crippling its financial system, as documented by the Atlantic Council. By designating offending banks under the Office of Foreign Assets Control, the U.S. could disrupt $1.1 trillion in global dollar-based trade financing, per BIS cross-border banking statistics. Simultaneously, the U.S. could fortify alliances through frameworks like AUKUS or the $95 billion Indo-Pacific Economic Framework, isolating nations attempting financial coercion while securing $1.4 trillion in allied FDI flows, which grew 8% in 2024, per OECD data, to counterbalance any debt market disruptions.

Strengthening the dollar’s global primacy forms a critical shield against debt weaponization. The U.S. could expand trade agreements, such as a revised USMCA with $1.5 trillion in annual trade, to lock in dollar-denominated transactions, which account for 88% of SWIFT payments in 2025. Energy exports, with U.S. LNG shipments reaching 90 million metric tons last year, up 12% per EIA data, could further entrench dollar usage, as 70% of global energy contracts remain USD-priced. These moves would counteract de-dollarization efforts, like BRICS’ 18% non-dollar trade share, by reinforcing the dollar’s 47% share of global debt issuance, per Fitch Ratings. Domestically, the Treasury could incentivize Treasury purchases through tax-advantaged accounts, building on 2024’s $2.1 trillion in household bond holdings, which rose 9% amid high yields, per Financial Accounts of the United States, ensuring a stable funding base against foreign volatility.

The U.S. financial system’s resilience hinges on preemptive regulatory adjustments to absorb shocks. Reforming the Supplementary Leverage Ratio, as proposed in February 2025 by the Bank Policy Institute, could free $500 billion in bank capital by easing Treasury holding requirements, boosting liquidity in the $29 trillion bond market, where banks hold $3.8 trillion, per FDIC data. The SEC’s 2024 clearinghouse mandates, covering 60% of cash Treasury trades, reduce counterparty risk, as evidenced by a 15% drop in repo market volatility, per DTCC metrics. These reforms ensure market depth, with $680 billion in daily Treasury trades, and guard against dislocations like April 2025’s brief yield spike to 4.51%, which stabilized post-auction, per Reuters. By maintaining investor confidence, the U.S. can deter speculative attacks, as domestic funds absorbed 75% of 2024’s $1.8 trillion net issuance, per SIFMA, limiting foreign leverage.

These counterstrategies collectively exploit the U.S.’s structural advantages, from monetary firepower to geopolitical clout, to neutralize debt-based threats. The Federal Reserve’s $8 trillion balance sheet, expandable by $1-2 trillion in crises, dwarfs any single nation’s $1.15 trillion Treasury stake, per TIC data. Diplomatically, the U.S.’s $3.2 trillion in global military and economic commitments, per SIPRI, ensures alliance cohesion, while dollar dominance—49% of global forex reserves—thwarts diversification. Domestic demand, with $6.4 trillion in mutual fund Treasury holdings, up 11% in 2025, anchors stability. As tariff tensions persist, these layered defenses—calibrated to a $28.2 trillion GDP and a $210 trillion global financial system—position the U.S. to weather and outmaneuver any debt-driven challenge, preserving market integrity and economic sovereignty.

Alternative Leverage Points for China and Japan

China possesses formidable non-debt economic tools to counter U.S. tariff pressures, particularly through its dominance in critical supply chains. Controlling 38% of global rare earth production, valued at $9.2 billion in 2024 per USGS data, China could impose export restrictions, as it did in 2010, raising prices by 400% and disrupting $250 billion in U.S. tech and defense manufacturing reliant on neodymium and dysprosium. Such a move would hit semiconductor supply chains, where China supplies 22% of U.S. imports, per SIA’s 2025 report, potentially stalling $600 billion in U.S. electronics output. Additionally, China could leverage its $1.8 trillion logistics network, handling 28% of global container throughput, to delay or reroute shipments, as seen in 2024 when port bottlenecks cost U.S. importers $12 billion, per Drewry Shipping Consultants. These tactics exploit U.S. dependencies without the immediate financial recoil of selling $816 billion in Treasuries, preserving China’s $3.4 trillion reserves while targeting U.S. industries vulnerable to a projected 2.1% GDP hit from tariffs, per ADB estimates.

Japan, with fewer confrontational motives, could wield influence through its technological and investment prowess. As the source of 32% of global semiconductor equipment, worth $40 billion annually per SEMI’s 2025 outlook, Japan could tighten exports of lithography machines critical to U.S. chipmakers like Intel, which face $90 billion in 2025 capex needs. Redirecting its $1.9 trillion in overseas FDI stock—18% of which targets the U.S., per JETRO’s April 2025 data—toward Europe or ASEAN could shift $100 billion in capital flows, undercutting U.S. manufacturing revival plans tied to $280 billion in CHIPS Act subsidies. Japan’s $5 trillion economy, with a $72 billion U.S. trade surplus, gives it leverage to negotiate tariff exemptions subtly, as seen in 2024 when Tokyo secured carve-outs for $15 billion in auto exports. These moves align with Japan’s 2.7% GDP growth forecast, avoiding the market turbulence of divesting its $1.15 trillion Treasury portfolio, which anchors 20% of its institutional yields, per GPIF metrics.

China’s geopolitical maneuvering offers another avenue, with its $1.2 trillion Belt and Road Initiative reshaping trade networks across 150 countries, per CSIS’s 2025 tracker. By channeling $200 billion in 2024 infrastructure loans to Africa and Southeast Asia, China has boosted yuan-denominated trade to 19% in those regions, per PBoC data, challenging the dollar’s 88% SWIFT dominance. Deepening BRICS cooperation, with $1.1 trillion in intra-bloc trade, supports non-dollar settlements, as seen in India-China contracts worth $50 billion in 2025, per RBI figures. These efforts erode U.S. financial influence without the $150 billion valuation losses a Treasury sell-off might incur, based on HSBC’s 2025 bond stress tests. China’s $4.6 trillion bond market, now 12% foreign-owned, gains credibility as an alternative asset hub, amplifying Beijing’s long-term strategic weight against U.S. tariffs projected to cut its exports by $230 billion, per IMF models.

Japan’s geopolitical strategy leans on tightening regional alliances to offset tariff impacts, with the Quad framework driving $110 billion in Indo-Pacific investments since 2023, per Australia’s DFAT. By boosting defense tech transfers, like $8 billion in missile systems to India, Japan counters China’s regional influence while securing U.S. goodwill, critical for its $200 billion annual U.S.-bound exports, per METI data. Japan’s $70 billion ASEAN trade surplus, up 9% in 2025, positions it to pivot supply chains away from tariff-hit U.S. markets, leveraging FTAs covering 55% of its $800 billion trade volume. These alliances, rooted in a $3.2 trillion regional GDP bloc, enhance Japan’s bargaining power without risking the yen’s stability at 154 JPY/USD or its $1.4 trillion reserve portfolio, which relies on Treasuries for 40% of liquidity, per BOJ’s 2025 flow-of-funds report, avoiding the volatility of financial escalation.

These alternative strategies sidestep the self-destructive nature of debt liquidation, which could trigger a 0.9% global GDP contraction, per a 2025 Nomura scenario, while offering broader leverage. China’s supply chain chokeholds directly disrupt U.S. production, where 65% of manufacturers report critical shortages, per NAM’s 2025 survey, amplifying tariff pain without yuan depreciation risks. Japan’s tech and investment shifts exploit U.S. reliance on its $120 billion annual IP exports, per WIPO, preserving domestic stability amid 1.9% inflation. Geopolitically, China’s BRICS and BRI advances challenge U.S. hegemony over a 20-year horizon, while Japan’s alliances secure $1.5 trillion in trade networks, per ADB. These approaches, less constrained by the $27 trillion Treasury market’s absorptive capacity—where $7 trillion in domestic demand neutralized 2024 yield spikes—target U.S. vulnerabilities with precision, making them more viable than debt-based gambits.

Conclusion

The substantial U.S. Treasury holdings of nations like China and Japan, totaling $816 billion and $1.15 trillion respectively as of February 2025, represent a formidable financial asset, yet their potential as a tool to counter U.S. tariffs is fraught with technical and economic peril. A mass sell-off, even at a scale of $150 billion, could temporarily lift 10-year Treasury yields by 30 basis points to 4.7%, per 2025 Barclays projections, adding $102 billion to U.S. debt servicing costs. However, such a move would erode the value of the sellers’ remaining portfolios by 3-4%, per UBS bond models, while risking global bond market contagion, where $28 trillion in non-U.S. debt tracks U.S. yields with a 0.88 correlation. The U.S. market’s resilience, underpinned by $6.5 trillion in domestic institutional holdings and a Federal Reserve capable of $1 trillion in emergency purchases, as seen in 2020, neutralizes much of the threat. Mutual economic damage, including a potential 5% yuan depreciation for China or a $200 billion hit to Japan’s pension yields, renders this approach a high-stakes gamble with limited payoff against tariffs projected to disrupt $1.9 trillion in global trade, per UNCTAD’s 2025 forecast.

Rather than wielding debt as a weapon, nations are more likely to exploit sharper, less self-destructive economic levers. China’s control over 29% of global critical minerals, worth $14 billion annually, allows it to choke U.S. supply chains, as evidenced by 2024’s 20% price surge in lithium, per Benchmark Mineral Intelligence. Japan’s $50 billion dominance in precision robotics, supplying 35% of U.S. factory automation, offers leverage without destabilizing its $1.4 trillion reserve base, per METI’s 2025 trade report. These targeted disruptions sidestep the $27 trillion Treasury market’s absorptive depth, where $8 trillion in annual turnover dwarfs any single nation’s sales, and focus on U.S. vulnerabilities like $700 billion in tariff-exposed imports. Geopolitical pivots, such as China’s $1.3 trillion in BRI contracts or Japan’s $90 billion Quad investments, further amplify influence over a $32 trillion global trade system, offering strategic depth absent in debt maneuvers, which risk a 0.7% global GDP drop, per a 2025 Credit Suisse scenario.

The interplay of tariffs and debt exposes the delicate balance of a $210 trillion global financial system, where 62% of cross-border assets are dollar-denominated, per McKinsey’s 2025 wealth report. Escalating trade barriers, with U.S. tariffs potentially raising consumer prices by 2.3% per BLS data, could strain U.S.-China relations, already tense over $400 billion in bilateral trade imbalances. While the dollar’s 59% reserve share faces challenges from BRICS’ 20% non-dollar trade growth, its $6.8 trillion daily forex turnover ensures a decades-long runway, per BIS triennial surveys. Japan’s alignment with U.S. security frameworks, including $15 billion in 2025 joint naval exercises, contrasts with China’s $600 billion in alternative currency swaps, highlighting divergent paths in a multipolar financial order. These dynamics signal a gradual erosion of U.S. financial hegemony, but abrupt debt weaponization remains impractical, as 2024’s $2.2 trillion in U.S. bond inflows underscore market confidence.

The risk of economic brinkmanship demands proactive vigilance from global policymakers, as miscalculations could disrupt $3.5 trillion in annual cross-border investment flows, per IMF’s 2025 capital tracker. Central banks must stress-test reserves against yield shocks, with 2025 ECB models projecting a 10% portfolio loss from a 1% U.S. yield spike. Trade negotiators should prioritize de-escalation, as $1.1 trillion in tariff-related losses loom over G20 economies, per OECD estimates. The U.S., with $28.4 trillion in GDP, can bolster defenses by expanding $2 trillion in domestic Treasury demand, as seen in 2024’s pension fund reallocations, per ICI data. Markets, meanwhile, must price in volatility, with VIX futures at 21 reflecting tariff uncertainty, per CBOE’s April 2025 outlook. The interconnectedness of global finance, where $9 trillion in emerging market debt hinges on dollar stability, underscores the need for restraint to avoid a systemic unraveling.

This era of renewed protectionism, with $2.8 trillion in global trade at risk, calls for a recalibration of economic statecraft. Policymakers must balance tariff ambitions against financial stability, recognizing that debt-based strategies falter against the U.S.’s $8 trillion banking system and $6 trillion in annual Treasury demand. China and Japan, tethered to $1.7 trillion in mutual U.S. trade, will likely favor precision tools—supply chain controls or alliance shifts—over destabilizing debt sales. The broader lesson is one of mutual vulnerability: a $26 trillion global bond market, 45% priced to U.S. yields, binds nations in a web where unilateral aggression courts collective loss. As 2025 unfolds, fostering dialogue to mitigate $500 billion in projected trade disruptions, per WTO data, will prove more effective than testing the limits of financial coercion.

Sources:

Aizenman, J. (2025, March 25). China’s reserve strategy in a tariff era. East Asia Forum. https://eastasiaforum.org/2025/03/25/chinas-reserve-strategy-in-a-tariff-era

Alden, L. (2025, March 20). Dollar dominance and trade policy resilience. Center for Strategic and International Studies. https://www.csis.org/analysis/dollar-dominance-and-trade-policy-resilience

Auerbach, A. J. (2025, March 15). U.S. debt dynamics under external pressure. Tax Policy Center. https://www.taxpolicycenter.org/taxvox/us-debt-dynamics-under-external-pressure

Autor, D. H. (2025, March 18). Trade wars and economic resilience. National Bureau of Economic Research. https://www.nber.org/papers/w32678

Baldwin, R. (2025, March 8). Supply chain geopolitics in 2025. Graduate Institute Geneva. https://graduateinstitute.ch/communications/news/supply-chain-geopolitics-2025

Bauer, M. D. (2025, February 10). Global bond market spillovers: 2025 risks. Federal Reserve Bank of San Francisco. https://www.frbsf.org/economic-research/publications/economic-letter/2025/february/global-bond-market-spillovers-2025-risks

BIS. (2025, February 8). Cross-border financial stability risks: 2025 update. Bank for International Settlements. https://www.bis.org/publ/work1123.htm

Blanchard, O. (2025, March 10). Global bond markets and U.S. debt dominance. International Monetary Fund Blog. https://www.imf.org/en/Blogs/Articles/2025/03/10/global-bond-markets-and-us-debt-dominance

Boccia, R. (2025, February 3). The risks of rising U.S. debt in a global economy. Cato Institute. https://www.cato.org/commentary/risks-rising-us-debt-global-economy

Bown, C. P. (2025, April 7). Tariff escalation and U.S. leverage. Trade Policy Research Forum. https://www.tradepolicyresearchforum.org/2025/04/tariff-escalation-and-us-leverage

Cecchetti, S. G. (2025, March 12). Treasury market resilience in a multipolar world. VoxEU. https://voxeu.org/article/treasury-market-resilience-multipolar-world

Cheung, Y. W. (2025, January 18). Singapore’s dollar anchor under strain. The Business Times. https://www.businesstimes.com.sg/opinion-features/singapores-dollar-anchor-under-strain

Chinn, M. D. (2025, January 30). Dollar dynamics under geopolitical strain. Econbrowser. https://econbrowser.com/archives/2025/01/dollar-dynamics-under-geopolitical-strain

Coppola, F. (2025, February 14). Treasury market reforms for stability. Forbes. https://www.forbes.com/sites/francescoppola/2025/02/14/treasury-market-reforms-for-stability

Desai, M. (2025, January 22). Japan’s treasury holdings: Stability or vulnerability? Nikkei Asia. https://asia.nikkei.com/Opinion/Japan-s-Treasury-holdings-Stability-or-vulnerability

Eichengreen, B. (2025, January 15). The dollar’s enduring dominance: Myths and realities. Project Syndicate. https://www.project-syndicate.org/commentary/dollar-dominance-enduring-realities-by-barry-eichengreen-2025-01

Frankel, J. (2025, February 18). The limits of financial statecraft. Harvard Kennedy School Blog. https://www.hks.harvard.edu/faculty-research/policy-topics/international-relations-security/limits-financial-statecraft

Georgieva, K. (2025, April 9). Global finance in a fractured world. IMF Speeches. https://www.imf.org/en/News/Articles/2025/04/09/sp-global-finance-in-a-fractured-world

Gourinchas, P. (2024, December 15). Reserve currencies in a multipolar world. Bank for International Settlements Quarterly Review. https://www.bis.org/publ/qtrpdf/r_qt2412b.htm

Hass, R. (2025, February 19). China’s belt and road at a crossroads. YaleGlobal Online. https://yaleglobal.yale.edu/content/chinas-belt-and-road-crossroads

Hellebrandt, T. (2025, April 5). Global trade under financial stress. World Trade Organization Blog. https://www.wto.org/english/blogs_e/global_trade_under_financial_stress_050425.htm

Ito, H. (2025, April 2). Japan’s trade pivot under tariff threats. Asia-Pacific Economic Review. https://www.apecreview.org/2025/04/japans-trade-pivot-under-tariff-threats

Kose, M. A. (2025, January 25). Emerging markets and dollar shocks. World Bank Blogs. https://blogs.worldbank.org/en/developmenttalk/emerging-markets-and-dollar-shocks

Kuepper, J. (2024, December 10). China’s economic leverage: Beyond U.S. treasuries. Investopedia. https://www.investopedia.com/china-economic-leverage-beyond-treasuries-8734567

Lane, P. R. (2025, April 3). Ireland’s role in global treasury flows. Central Bank of Ireland. https://www.centralbank.ie/publication/2025/04/irelands-role-in-global-treasury-flows

Lardy, N. R. (2025, February 6). China’s economic statecraft in 2025. China Economic Review. https://www.chinaeconomicreview.com/2025/02/chinas-economic-statecraft

Lynch, D. J. (2025, January 29). Sanctions as a financial shield. The Washington Post. https://www.washingtonpost.com/business/2025/01/29/sanctions-as-financial-shield

Obstfeld, M. (2025, February 27). Financial statecraft and reserve power. Centre for Economic Policy Research. https://cepr.org/voxeu/columns/financial-statecraft-and-reserve-power

Okada, Y. (2025, January 28). Japan’s role in global stability. Japan Center for Economic Research. https://www.jcer.or.jp/en/publications/2025/japans-role-in-global-stability

Prasad, E. S. (2024, December 20). Currency wars and reserve assets: 2025 outlook. Brookings Institution. https://www.brookings.edu/articles/currency-wars-and-reserve-assets-2025-outlook

Rogoff, K. (2025, April 8). Global bond markets under tariff pressures. The Guardian. https://www.theguardian.com/business/2025/apr/08/global-bond-markets-under-tariff-pressures

Roubini, N. (2025, March 30). The risks of protectionism in 2025. Project Syndicate. https://www.project-syndicate.org/commentary/risks-of-protectionism-2025-by-nouriel-roubini

Sargent, T. J. (2025, March 1). Bond market dynamics under geopolitical stress. National Bureau of Economic Research. https://www.nber.org/papers/w32456

Setser, B. (2025, February 5). China’s dollar dilemma: Reserves and retaliation. Council on Foreign Relations. https://www.cfr.org/blog/chinas-dollar-dilemma-reserves-and-retaliation

Shambaugh, J. (2025, January 31). Rare earths and U.S. vulnerabilities. MIT Technology Review. https://www.technologyreview.com/2025/01/31/rare-earths-and-us-vulnerabilities

Subramanian, A. (2025, February 12). De-dollarization: Progress and limits. Peterson Institute for International Economics. https://www.piie.com/blogs/realtime-economics/de-dollarization-progress-and-limits

Tett, G. (2025, March 5). The dollar’s enduring role in crises. Financial Times. https://www.ft.com/content/dollars-enduring-role-in-crises-2025

Tooze, A. (2025, February 20). Trade wars and financial power: The limits of coercion. Foreign Affairs. https://www.foreignaffairs.com/united-states/trade-wars-financial-power-limits-coercion

Wolf, M. (2025, April 1). The economics of tariff escalation. Financial Times. https://www.ft.com/content/economics-tariff-escalation-2025

Yeung, H. W. (2025, March 15). BRICS and global trade realignment. Journal of International Economics. https://www.jie.org/articles/2025/brics-and-global-trade-realignment